This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As cryptocurrency gains popularity and central bank digital currencies ( CBDCs ) are explored globally, major financial institutions are undergoing significant transformations to adapt to this new landscape. Central banks worldwide are exploring the potential of CBDCs as digital versions of their national currencies.

Artificial intelligence (AI) is transforming industries across the globe, and banking is no exception. The adoption of AI is revolutionizing banking products, enabling financial institutions to offer personalized service, increase efficiency, and enhance security. AI-Driven Innovations in Banking Products 1.

And its transforming how businesses operate. From writing assistance to automated data analysis, LLMs enable users to work more efficiently, thereby freeing up time to focus on higher-value tasks. According to Accenture , more than 50% of work in the banking sector has a high potential for automation.

How do banks make money? What is a bank really worth? Firstly, by outlining the major items on a bank’s income statement, and then by discussing key ratios that are commonly used to measure profitability and to estimate the market value for banks. Where does this money ultimately go? the spread).

When it comes to tech innovations, the banking sector is usually ahead of the curve. Banks are buzzing with excitement over Gen AI, and its future in the sector looks even brighter. Banks are buzzing with excitement over Gen AI, and its future in the sector looks even brighter.

In the previous article , we looked at how banks make money and how they must meet capital requirements. In this article, we will explore the importance of profitability ratios and valuation metrics that are crucial when analyzing banks. It provides insights into how effectively a bank utilizes shareholder capital to generate profits.

Despite many current applications being small-scale pilot projects, the promise of Gen AI to revolutionise bankingoperations and enhance customer experiences is becoming clear. This helps banks to quickly identify profitable investment opportunities and risks so as to maximise investment returns and minimize losses.

While Gen AI holds big promise for banking , most of the current deployments are limited to just a few areas or don’t go beyond the experimental phase. Though early pilots appear impressive, it will definitely take time to realize Gen AI’s full potential for the banking industry. Five Challenges for AI in the Banking Sector 1.

Today, I want to introduce you to (or perhaps remind you of) the concept of the minimum efficient scale. It is the notion that, as a company gets bigger, it is able to achieve cost savings through its “scale” or the size of its operations. The concept of “minimum efficient scale” is less well known and is a less-used term.

Smart, always-connected devices and anytime/anywhere interactions are now givens, particularly among millennials, who expect such conveniences in banking and financial services. Mapping this group to its customer base, the bank can make targeted offers to customers who could be in the home or auto market in the next 30 to 90 days.

For all the angst over the disruptive impact of financial technology providers, the smart money in corporate banking sees fintechs as strategic allies, not enemies. Over the past decade, the fintech market has become a hotbed of customer-centric banking innovation.

Before we dive into why AI is the solution for the banking sector, let’s first explore what big tech companies have in common, how many of them have grown successfully, and what banks can learn. Usage of AI in the Banking Sector. Table 1: AI applications across Canadian and US banks (Source: Financial Post, Techemergence).

In the digital age, businesses are constantly seeking innovative ways to gain a competitive edge and streamline their operations. From enhancing customer experiences to optimizing decision-making processes, AI is reshaping the way businesses operate and opening up new possibilities for growth.

After building a successful model in financial services, Oliver Wyman expanded to offer pure strategy consulting services to non-financial services groups and now has 2 internal divisions that operate relatively independently. Corporate and Institutional Banking. Retail and Business Banking. Oliver Wyman became own firm again.

Just over 10 years ago, French bank BNP Paribas froze U.S. There was a run on British bank Northern Rock. Over the next year, many banks fell. Investment bank Bear Stearns collapsed. We expect investment banks to embark on an even more fundamental makeover during the next decade. The New Face of Investment Banks.

The Business of Banking. Banks are intermediaries for capital and hold the risk when supply and demand is not perfectly balanced. Commercial Banking. A bank, on the other hand, can diversify this credit risk and reduce the average cost of vetting each loan by lending to many borrowers. Investment Banking.

BCG’s Retail-Banking Excellence benchmarking study (REBEX) profiles the operational and digital practices and performance of 20 of the world’s leading retail banks, a group of 40 institutions chosen for their size and the strength of their capabilities. We refer to these banks as the “premier league.”

The consumer banking industry is notoriously difficult to enter, not least because most customers rarely switch banks. In some countries, people change spouses more often than they change banks. It has now become the largest bank in the country. These areas were underserved by the traditional banks.

It operates at the task level and not the end-to-end process level.” The company may have collections of standard operating procedures, but they are often poorly documented and out of date. health care firm, for example, had over the years stripped a process down to the minimal viable steps to achieve efficiencies.

Small startup firms are already developing proprietary technologies — such as machine vision, deep learning, and other innovations —– that could help large investors evaluate opportunities and risks with far greater accuracy and efficiency than was previously possible.

We analyzed companies’ debt-to-equity ratio, equity ratio, risk buffer, property mortgage or the mortgage of the venture’s real estate ratio, the use of bank overdraft facilities/approved checking account ratio, and long-term liabilities or loans ratio. Risk-taking.

FinTechs are internet companies that streamline financial systems and make funding the supply chain more efficient. They include new enterprises such as Orbian , Prime Revenue , C2FO , Taulia , and Ariba as well as new operations launched by traditional financial service firms such as Citi Group, HSBC, BNP Paribas, and Deutsche Bank.

And yet front-line employees are still often left operating with data that’s “too little, too late.” Data is not always shared efficiently. Another example comes from Royal Bank of Scotland (RBS). For example, analytics helped the bank identify customers that were in need of financial advice.

My perspective and approach to misconduct risk are influenced by my work as a bank supervisor, and by my background and training as an economist. In my view, bank supervision must include attention to the culture at financial firms, not just to their financial safety and soundness.

The value of bank branches, for example, is no longer to manually process deposits, but to solve more complex customer problems like providing mortgages. Once a task becomes automated, it also becomes largely commoditized. Value is then created on a higher level than when people were busy doing more basic things. market share in online sales.

Since the advent of Bitcoin in 2008, digital currency has been a growing trend and a growing area of interest for consultants, businesses, fintech investors, central banks, and governments. Digital currency vs electronic banking. Another difference is that electronic banking involves interacting with the banking system.

Meanwhile, according to the Ministry of Finance , the Indian economy is operating with $45 billion less cash than it did prior to demonization. Since then, the government has created more than 300 million new, no-frills bank accounts. A year later, after demonetization, the same system is processing 76 million transactions per month.

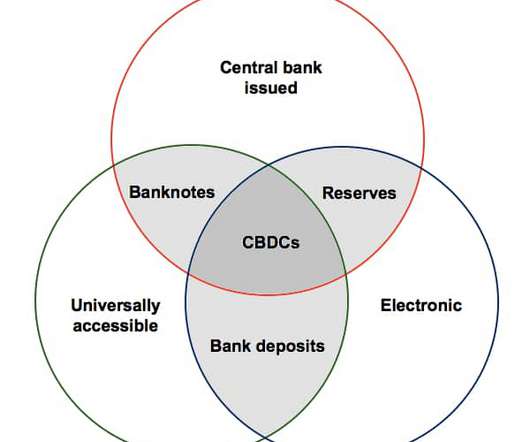

Central Bank Digital Currencies (CBDCs) are a new form of digital currency that will be issued and backed by central banks. While CBDCs and bank deposits can both be transferred digitally, there are at least five key differences between CBDCs and bank deposits that are worth being aware of.

When a bank suffers a physical robbery, we do not think of blaming and shaming it – even though there is almost always some additional precaution the bank could have taken that might have helped prevent the attack (such as a police officer stationed at every teller window or limiting customer access to tellers).

Your employer operates with the express aim of benefiting members of the community and reinvests all profits to further its social aims. Imagine waking up in a world where you feel positive and motivated about going to work, knowing that your work provides value to customers in a way that is sustainable and responsible.

Why you need a COO or Operations Manager. Either their operations have grown quite a bit or they are in the midst of growing. Many founders and CEOs ask us this question: Do I need an operations manager? But there are a few questions: Why is it necessary to hire an operations person? We answer with a resounding yes.

Let’s start by examining the potential effects of this on an industry that touches all of our lives – banking. The banking industry is filled with shared resources. Instead, the technology itself would do the heavy lifting of uniting the interests and business processes of the member banks.

International trade has tripled as a share of global GDP since 1945, and banks have done well from it. Documentary trade, traditionally facilitated by letters of credit (LCs) issued by banks, is steadily being replaced by open-account trade. Banks must be prepared to respond to rapid changes in the quantity and location of demand.

How do banks switch customer relationships from branch offices to mobile phone screens? For every company wrestling with evolutions in its strategy, success depends as much on matching the operating model to those evolutions as it does on the soundness of the strategy itself. sweetvenom/Getty Images. Insight center.

. “To prosper over time,” he argued, “companies must benefit all of their stakeholders, including shareholders, employees, customers, and the communities in which they operate.” billion of India’s citizens to voting, banking, government assistance, healthcare, recordkeeping, and more.

In Precision’s case, good tactical performance required developing rules, checklists, and standard operating procedures and then following them closely. A great salesperson will operate much more efficiently with a defined process for reaching out to prospects. We made a number of operational changes to the call center.

Recently, the CEO of Deutsche Bank predicted that half of its 97,000 employees could be replaced by robots. ” Machine learning algorithms are also predicted to replace people responsible for “optical part sorting, automated quality control, failure detection, and improved productivity and efficiency.”

Immutability and security are vital to the operation of government and business due to the sensitive information these institutions gatekeep. Low transaction costs will also be necessary to ensure efficientoperations and to ensure that blockchain systems offer a cost advantage over the status quo.

We find it useful to start with four qualities most executives want their organizations to have: responsiveness, reliability, efficiency, and perennity (e.g., For some tasks, it is desirable or necessary to have common rules across the operating units: policies, standards, methods, procedures, or systems. Minimum efficient scale.

Although mobile payments make the life of the consumer easier, they pose a major challenge for banks and other financial institutions who now face high competition from the financial technology companies (fintechs) that led this transition to mobile P2P payments. Venmo, a mobile transfer system favored by millennials in the U.S.,

But what are the challenges that IT leaders are encountering as they try to keep pace and try to transform process and operations while the business is evolving? Driving digital transformation really means driving rapid, efficient, and high-ROI responses to those changes. Let’s take banking, for example. Max De Ycaza, IBM.

Priorities might include developing new products, expanding into new markets, enhancing the customer experience, increasing operationalefficiency, or embracing sustainability. Economies of scale – For example, McDonald’s enjoys large cost advantages due to its scale of operation.

And that’s not just social media accounts; it’s bank accounts, retailer gift card accounts with cash and credit cards attached, airline loyalty accounts with years of accumulated frequent flyer points, and other accounts with real value. Over three billion credentials were reported stolen last year.

When I first joined BNP Paribas Fortis, for example, two younger and more dynamic banks had just overtaken us. The bank was using a project management tool, but the lack of discipline in keeping it up to date made it largely fruitless. What about efficiency? Every organization needs what I call a “hierarchy of purpose.”

We organize all of the trending information in your field so you don't have to. Join 55,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content