This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

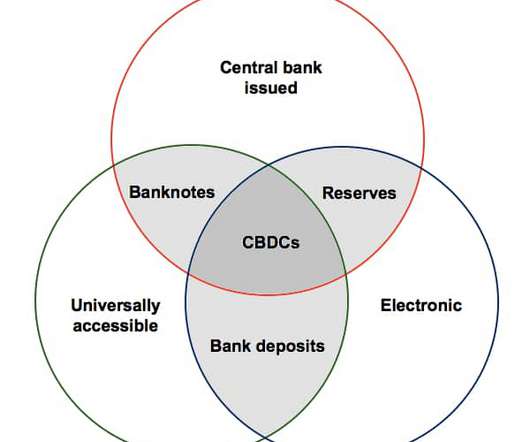

As cryptocurrency gains popularity and central bank digital currencies ( CBDCs ) are explored globally, major financial institutions are undergoing significant transformations to adapt to this new landscape. Central banks worldwide are exploring the potential of CBDCs as digital versions of their national currencies.

Artificial intelligence (AI) is transforming industries across the globe, and banking is no exception. The adoption of AI is revolutionizing bankingproducts, enabling financial institutions to offer personalized service, increase efficiency, and enhance security. AI-Driven Innovations in BankingProducts 1.

For product leaders , large language models (LLMs) arent just another shiny tech trend, theyre reshaping how businesses interact with customers, automate workflows, and make decisions. According to Accenture , more than 50% of work in the banking sector has a high potential for automation. And its transforming how businesses operate.

In todays fast-paced, customer-centric marketplace, developing successful products requires more than just technical skills and innovation it demands a deep understanding of users’ needs and a creative approach to problem-solving. What is Design Thinking? These stages are not linear.

It’s been more than 25 years since Bill Gates dismissed retail banks as “dinosaurs,” but the statement may be as true today as it was then. Banking for small and medium-sized enterprises (SMEs) has been astonishingly unaffected by the rise of the Internet.

Like the internet, this technology is designed to be decentralized, with “layers,” where each layer is defined by an interoperable open protocol on top of which companies, as well as individuals, can build products and services. The TCP/IP protocol was used to address and control how packets of data were routed between computers.

Open banking is transforming the financial industry , promising greater transparency, competition, and innovation. The European Union, which looks set to introduce updated rules about digital payments and financial services within the next two years, is at the leading edge of regulating open banking. What is Open Banking?

When my daughters were little, each time one of them received a birthday or holiday card from their grandparents with a crisp $20 in it, I silently vowed that I would finally get around to opening a savings account for them at our local bank so they could start learning the virtues of saving and compounded interest. That got old quickly.

How do banks make money? What is a bank really worth? Firstly, by outlining the major items on a bank’s income statement, and then by discussing key ratios that are commonly used to measure profitability and to estimate the market value for banks. Where does this money ultimately go?

That’s our product, and that’s our passion. It launched a product, gathered feedback, and kept iterating as it scaled and added users. At the other is a product or service that solves the problem or addresses the market in a way nobody has thought of before. Your data isn’t even in the picture.

Despite many current applications being small-scale pilot projects, the promise of Gen AI to revolutionise banking operations and enhance customer experiences is becoming clear. This helps banks to quickly identify profitable investment opportunities and risks so as to maximise investment returns and minimize losses. Risk Management 3.1

Smart, always-connected devices and anytime/anywhere interactions are now givens, particularly among millennials, who expect such conveniences in banking and financial services. Organizations have always collected data on customers, suppliers, products, and services. Digital is reconfiguring the world.

Before we dive into why AI is the solution for the banking sector, let’s first explore what big tech companies have in common, how many of them have grown successfully, and what banks can learn. Usage of AI in the Banking Sector. Table 1: AI applications across Canadian and US banks (Source: Financial Post, Techemergence).

Product managers have a dynamic role within companies, sitting at the intersection between business leaders, customers, engineers, and designers. They help to organize the development process so that products meet customer needs and business goals. What is a Product? Managing the Product Lifecycle.

Consumers are no longer swayed by just a great product, but seek more than that, craving authenticity and a genuine connection to the brand. Indeed, the battle to build brand loyalty requires more than just great products. She has a strong passion for strategy consulting, investment banking, business, and entrepreneurship.

Much has been made of the fact that a new breed of financial technology (or fintech) companies is unbundling banks in the developed world. Startups are attacking all of the components of the traditional bank value proposition (e.g., Sidian Bank in Kenya has a similar program. However, there are signs that this is changing.

Remember this: If your customers want to use your product, make it easy for them to do so. Because product problems cause several other problems: The customers have to decide if the aggravation of using this product outweighs the defects. Customers will not wait forever for you to fix problems in your product.

For populations living so far off the economic grid that traditional banks have never considered them as a source of new business, the availability of mobile technology is lifting the bane of cash dependency and opening a door to the mainstream of the global economy.

After a close look at workplace policies across corporations, banks, law firms, and tech companies, the New York Times called grueling competition the defining feature of the upper-echelon workplace. Some of the behaviors we asked about were creative, such as “Search out new technologies, processes, techniques, and/or product ideas.”

Basically, a handful of asset management firms have become the most powerful shareholders of the nation’s largest banks. In “ Ultimate Ownership and Bank Competition ,” José Azar, Sahil Raina, and I looked at banks across different parts of the United States. Take a look at this table.

But this is the story of how a group of bank examiners at the Federal Reserve Bank of Philadelphia, one of 12 banks in the U.S.’s The 250 people in the supervision, regulation, and credit group at the Philadelphia bank supervise the commercial and retail banks based in their district.

Sometimes a fieldstone is too big for me, so I use the notion of an “idea bank.” ” My idea bank reminds me of themes I want to possibly address in the future. The Blank Page Problem Can Stop Writers from Writing Before I knew about fieldstones or the idea bank, I had trouble starting a piece.

In the face of this dynamic, it isn’t enough to create new products and services. Unless we also design new ways of talking about ideas and exploring the future, those product and service innovations will never be embraced by the organization and never make their way out into the world. Designing the New Product.

What are the Benefits of Learning & Development Programs for Organizations When you’re spending the time and money training employees, you want to ensure that you’re getting the best bank for your buck–that’s where learning and development programs come in.

Instead, you’re left with less money in the bank and employees mindlessly clicking through the lessons, just praying for it to end. eLearning can save you time and money while also improving productivity, increasing employee retention, and more. That’s where eLearning comes in.

They seized this opportunity to establish a firm that would help firms gain clarity about their business models, products, and clients and then advise them by creating long term strategies. Industrial Products. Retail and Consumer Products. Corporate and Institutional Banking. Retail and Business Banking.

Let’s start by examining the potential effects of this on an industry that touches all of our lives – banking. The banking industry is filled with shared resources. Instead, the technology itself would do the heavy lifting of uniting the interests and business processes of the member banks.

As I discussed in another post, Brad Staats of the University of North Caroline at Chapel Hill and I demonstrated the success of these approaches by analyzing 2 ½ years of transaction data from a unit at a Japanese bank that processes applications for home loans. Others did not watch such videos (our control condition).

Since the advent of Bitcoin in 2008, digital currency has been a growing trend and a growing area of interest for consultants, businesses, fintech investors, central banks, and governments. Digital currency vs electronic banking. Another difference is that electronic banking involves interacting with the banking system.

For example, as it grew, Facebook found that its early “move fast and break things” culture had to be funneled into focused technical teams and product groups to make its product development process faster and less erratic, and for it to have a chance of meeting the demands of its new public shareholders following its IPO.

My perspective and approach to misconduct risk are influenced by my work as a bank supervisor, and by my background and training as an economist. In my view, bank supervision must include attention to the culture at financial firms, not just to their financial safety and soundness. The economics of corporate culture. Externalities.

Bear in mind that the opioid scandal events were unfolding roughly in parallel to the banking scandals where banking institutions paid out billions of dollars for misconduct allegations. As a quick reminder – banking financial advisors were selling unneeded financial instruments in order to meet their sales quotas.

On March 10th, Silicon Valley Bank went bankrupt. Due to the Federal Reserve’s determination to curb inflation it has consistently hiked interest rates for the last 12 months, an outcome that SVB and many other banks failed to anticipate. As the size of SVB’s losses became known, this startled anyone with money in the bank’s coffers.

“Productivity isn’t everything, but in the long run it is almost everything,” wrote Paul Krugman more than 20 years ago. Productivity in most developed economies has been anemic. During much of this time, it has been shareholders, not workers, who have reaped the benefits of higher productivity.

Self-cannibalization occurs when a company chooses to proactively replace one product or process with another that is potentially worth less. Forward-looking incumbents recognize the need to cannibalize their own products, rather than leaving it to other startups, who are more than happy to take on the challenge.

These systems can suggest relevant products that customers are likely to enjoy. For example, Alibaba, a leading Chinese e-commerce company, could conduct sentiment analysis of customer reviews of individual products and services, and use these insights to modify existing products and develop new ones.

When the policy change was announced, people were given until December 30, 2016, to return 500- and 1,000-rupee notes to banks, or else risk losing the value of them. According to a Bloomberg report , banks were estimated to have received 14.97 trillion rupees (around $220 billion) by the December 30 deadline, or 97% of the 15.4

Companies born before the internet took hold have an enormous challenge: improving their online products and services at the warp speed of their online competitors. Virtual financial services firms such as Wealthfront and Betterment are siphoning investments from established banks through a great mobile app and a website.

For example, one driver suggested new products like Gogurts and fun string cheese that parents could get delivered early and pop into their kids’ lunches before school. The employee attrition ratio, which had been the highest among all of the foreign banks in China, was reduced to the lowest among all foreign banks in China.

Innovate a product or service from within your position. In 1979 interest rates skyrocketed, rising to over 20%, causing real pain in the banking industry.

The prize for best answer was a FREE Consulting Case Bank and The Consulting Bible 3rd edition – a HUGE giveaway – so we weren’t surprised when we heard from so many of you. For instance, we examined predatory pricing in the airline industry and illegal product tying by Apple, Microsoft, and AT&T. We love it!

They include new enterprises such as Orbian , Prime Revenue , C2FO , Taulia , and Ariba as well as new operations launched by traditional financial service firms such as Citi Group, HSBC, BNP Paribas, and Deutsche Bank. The use of FinTechs allows suppliers to access funding at the multinationals firm’s lower cost of capital.).

.” Vernon Hill, an entrepreneur whose young company, Metro Bank, is reshaping the future of financial services in the UK , exudes a spirit of energy and confidence that is infectious. But it’s the mindset he personifies that defines the fast-growing bank. The Eager Experimenter. Are you that kind of leader?

Recently, the CEO of Deutsche Bank predicted that half of its 97,000 employees could be replaced by robots. ” And for those in manufacturing or production companies, the future may arrive even sooner. ” The point of technology, she argues, is to boost productivity, not cut the workforce. Insight Center.

We organize all of the trending information in your field so you don't have to. Join 55,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content