This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

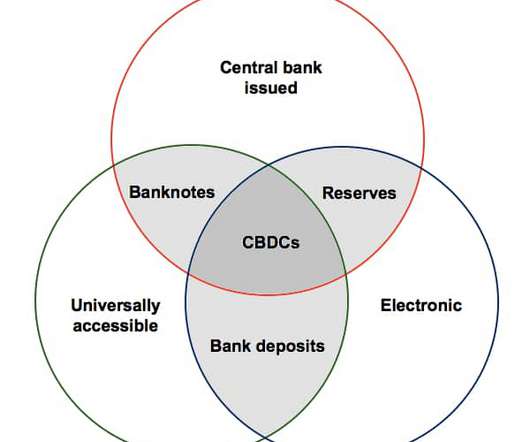

As cryptocurrency gains popularity and central bank digital currencies ( CBDCs ) are explored globally, major financial institutions are undergoing significant transformations to adapt to this new landscape. Central banks worldwide are exploring the potential of CBDCs as digital versions of their national currencies.

Artificial intelligence (AI) is transforming industries across the globe, and banking is no exception. The adoption of AI is revolutionizing banking products, enabling financial institutions to offer personalized service, increase efficiency, and enhance security. AI-Driven Innovations in Banking Products 1.

Employing a team of strong workers can help you get through these unknown times, which is why investing in employee development is crucial. Learning new skills and competencies is the bread and butter of a learning and development program. The more training you offer, the more efficient and effective employees are in a role.

Why LLMs Matter for Product Leaders For product leaders, LLMs are revolutionizing product development by making it possible to build and deploy more intelligent, personalized, responsive, and accessible digital applications that enhance overall customer satisfaction. Here are three key challenges to consider.

When it comes to tech innovations, the banking sector is usually ahead of the curve. Banks are buzzing with excitement over Gen AI, and its future in the sector looks even brighter. Banks are buzzing with excitement over Gen AI, and its future in the sector looks even brighter.

While Gen AI holds big promise for banking , most of the current deployments are limited to just a few areas or don’t go beyond the experimental phase. Though early pilots appear impressive, it will definitely take time to realize Gen AI’s full potential for the banking industry. Five Challenges for AI in the Banking Sector 1.

Despite many current applications being small-scale pilot projects, the promise of Gen AI to revolutionise banking operations and enhance customer experiences is becoming clear. This helps banks to quickly identify profitable investment opportunities and risks so as to maximise investment returns and minimize losses. Risk Management 3.1

Before we dive into why AI is the solution for the banking sector, let’s first explore what big tech companies have in common, how many of them have grown successfully, and what banks can learn. Usage of AI in the Banking Sector. Table 1: AI applications across Canadian and US banks (Source: Financial Post, Techemergence).

For all the angst over the disruptive impact of financial technology providers, the smart money in corporate banking sees fintechs as strategic allies, not enemies. Over the past decade, the fintech market has become a hotbed of customer-centric banking innovation.

This confusion originates in the fact that for older forms of money — gold or bank notes — there is no distinction between the “what” and the “how”; you simply pay by handing dollar bills or gold coins to the seller. This made traditional banks in the U.S. This made traditional banks in the U.S.

Just over 10 years ago, French bank BNP Paribas froze U.S. There was a run on British bank Northern Rock. Over the next year, many banks fell. Investment bank Bear Stearns collapsed. We expect investment banks to embark on an even more fundamental makeover during the next decade. The New Face of Investment Banks.

Much has been made of the fact that a new breed of financial technology (or fintech) companies is unbundling banks in the developed world. Startups are attacking all of the components of the traditional bank value proposition (e.g., Lack of Infrastructure and Efficient Cloud Services.

In the meantime, Marsh & McLennan was creating Mercer; in 1975, Mercer was developed as the human resources consulting arm of Marsh & McLennan. The firm offers consulting services including strategy, operations, risk management, organizational transformation, and leadership development. Corporate and Institutional Banking.

The war certainly has prevented an efficient economic structure, forcing many Colombians to be inward-looking. “It’s a culture thing,” María Lacouture, the head of government economic development agency ProColombia, told me. We’d focus on, how can I develop in my area, in my business?”

Since the advent of Bitcoin in 2008, digital currency has been a growing trend and a growing area of interest for consultants, businesses, fintech investors, central banks, and governments. Digital currency vs electronic banking. Another difference is that electronic banking involves interacting with the banking system.

But this is the story of how a group of bank examiners at the Federal Reserve Bank of Philadelphia, one of 12 banks in the U.S.’s The 250 people in the supervision, regulation, and credit group at the Philadelphia bank supervise the commercial and retail banks based in their district.

For example, Alibaba, a leading Chinese e-commerce company, could conduct sentiment analysis of customer reviews of individual products and services, and use these insights to modify existing products and develop new ones. Zuhair Imaduddin is an Innovation Development Analyst at JPMorgan Chase.

bank CEOs who were born in the U.S., banks between 1994 and 2006. The banking industry experienced a series of profound competitive shocks in the 1990s. The one we used was the Interstate Banking and Branching Efficiency Act (IBBEA) of 1994 that legalized interstate branching in some U.S. For instance, U.S.

The most prominent CM fintechs have been strongly supported and engaged by the CM ecosystem, which includes players such as investment banks, custodians, exchanges, clearing-houses, and CM-focused information service providers.

What sets RPA apart from other automation technologies is that its ability to imitate a human user of one or more information systems reduces development time and extends the range of functions that can be automated across a much wider range of business activities. billion customer journey transformation program.

Case interviews go beyond just spouting business knowledge – you are tested on how you build and communicate a clear framework, break down problems into small pieces, develop real world options, and recommend actionable solutions despite the presence of conflicting information. For now, however, let’s just get started.

The value of bank branches, for example, is no longer to manually process deposits, but to solve more complex customer problems like providing mortgages. Once a task becomes automated, it also becomes largely commoditized. Value is then created on a higher level than when people were busy doing more basic things. ” she continues.

His views on digital transformations include his experience as a member of the research team that developed the first web browser (Mosaic, the predecessor to Netscape) in the early 1990s and as a technology entrepreneur. Since then, the government has created more than 300 million new, no-frills bank accounts.

FinTechs are internet companies that streamline financial systems and make funding the supply chain more efficient. They include new enterprises such as Orbian , Prime Revenue , C2FO , Taulia , and Ariba as well as new operations launched by traditional financial service firms such as Citi Group, HSBC, BNP Paribas, and Deutsche Bank.

We analyzed companies’ debt-to-equity ratio, equity ratio, risk buffer, property mortgage or the mortgage of the venture’s real estate ratio, the use of bank overdraft facilities/approved checking account ratio, and long-term liabilities or loans ratio. Risk-taking. Underperformance.

The partnership has been a triumph of efficiency — a win-win for the cultural climate of Judson and often-stretched student bank accounts. In a similar vein, a new group of innovators is finding efficiencies not in separating people by age but by bringing them together. But something else has happened.

Despite a tentative financial recovery, the retail-banking industry faces unrelenting, disruptive challenges. Banks that hope to prevail must urgently pursue digital simplicity. That mandate for digital simplicity is the central insight emerging from the research behind this sixth edition of BCG’s annual Global Retail Banking report.

Let’s start by examining the potential effects of this on an industry that touches all of our lives – banking. The banking industry is filled with shared resources. Instead, the technology itself would do the heavy lifting of uniting the interests and business processes of the member banks.

Recently, the CEO of Deutsche Bank predicted that half of its 97,000 employees could be replaced by robots. ” Machine learning algorithms are also predicted to replace people responsible for “optical part sorting, automated quality control, failure detection, and improved productivity and efficiency.”

Although mobile payments make the life of the consumer easier, they pose a major challenge for banks and other financial institutions who now face high competition from the financial technology companies (fintechs) that led this transition to mobile P2P payments. Venmo, a mobile transfer system favored by millennials in the U.S.,

When a bank suffers a physical robbery, we do not think of blaming and shaming it – even though there is almost always some additional precaution the bank could have taken that might have helped prevent the attack (such as a police officer stationed at every teller window or limiting customer access to tellers).

Hiring and developing great people to support you. Nonprofit Fundraising Events : Friends Asking Friends helps you empower your supporters, reach more people, and execute your fundraising events efficiently ? The Power to Choose The Freedom to Innovate. Listening to your feedback to improve our solutions.

As a startup founder, I’m constantly struggling to recruit top talent without breaking the bank. How do you recruit a developer making well into six figures, or an experienced salesperson with four kids in private school? Invest in training and professional development.

Governments, businesses, and individuals are developing new use cases for blockchain as barriers to adoption continue to decrease. Low transaction costs will also be necessary to ensure efficient operations and to ensure that blockchain systems offer a cost advantage over the status quo. In contrast, Singapore supports cryptocurrency.

We argue that, like previous revolutionary ideas, blockchain has the potential to help developing nations leapfrog more-developed economies. This in turn boosted development by allowing relatively poor farmers to reliably send and receive payments at affordable rates, fostering economic growth by lowering transaction costs.

And the pioneering work of social enterprises in sectors like construction , manufacturing , banking , hospitality and healthcare suggest that innovative and sustainable businesses are able to thrive without being run primarily for profit. In Canada, for example, these institutions now contribute 8% of the country’s GDP.

Removing the financial intermediary, i.e. the bank, can increase convenience, efficiency, and security. Traditionally this problem has been solved by sending payments through the banking system. However, what happens when banks manipulate financial records or simply collapse? The bottom line.

Recently though, some new companies have figured that, in today’s digital age, there are other and perhaps more efficient ways of matching clients with consultants: online, through search terms, and by building rich databases. And that’s how they have always done it. In fact, you cannot successfully do consulting without them.

Thus a trust and efficiency engine like blockchain technology has the potential to drive radical change in the insurance industry while improving transparency and outcomes across the entire value chain. And yet trust in business institutions, and the financial services sector in particular, is at an all-time low.

” A fintech start-up enjoyed greater success piloting a security offering with a global bank. The startup initially offered a similarly comprehensive approach, but the bank — driven by unhappy customer feedback — was interested in improving a particular aspect of the online user experience around security.

Productivity in most developed economies has been anemic. Beyond wages, other forms of investment in human capital include education and training, improved healthcare, and other, less obvious investments, such as the time and space to explore new ideas and professional development opportunities.

Driving digital transformation really means driving rapid, efficient, and high-ROI responses to those changes. Where our clients struggle and where we see challenges is not in the area of new product development. Can you talk a little about the development of agile for services and what that means to customers?

The inquiry relates to allegations that Tapie, a supporter of conservative former President Nicolas Sarkozy, was improperly awarded 403 million euros ($531 million) in an arbitration to settle a dispute with now defunct state-owned bank Credit Lyonnais. In the US, individuals other than Bernie Madoff and Martha Stewart don''t get prosecuted.

With automated pricing engines, insurers and banks can roll out new offers as fast as online competitors. Once processes critical to achieving an efficiency or goal are automated, managers need to develop structured analytics as well as centralize data processes so that the way data is collected is standardized and can be entered only once.

We organize all of the trending information in your field so you don't have to. Join 55,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content