This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As cryptocurrency gains popularity and central bank digital currencies ( CBDCs ) are explored globally, major financial institutions are undergoing significant transformations to adapt to this new landscape. 2024, the global cryptocurrency market capitalisation reached more than US$3.7

Artificial intelligence (AI) is transforming industries across the globe, and banking is no exception. The adoption of AI is revolutionizing banking products, enabling financial institutions to offer personalized service, increase efficiency, and enhance security. AI-Driven Innovations in Banking Products 1.

One answer lies in founder-led marketing, a relatively new concept, but one taking the social media world by storm. We can get a better understanding of how effective founder-led marketing can be by considering two recent success stories. In aB2Bcontext, your USP might focus on efficiency, cost savings, or technical performance.

In the previous article , we looked at how banks make money and how they must meet capital requirements. In this article, we will explore the importance of profitability ratios and valuation metrics that are crucial when analyzing banks. We will examine each in turn. All else being equal, a lower number is better.

A higher “Volume” of data has led to more efficient decision-making in numerous instances, such as in programmatic marketing and in banking. In the field of data-driven marketing, an answer to addressing this limitation lies in blockchain technology. Data-Driven Marketing. Distributed Database.

When it comes to tech innovations, the banking sector is usually ahead of the curve. Banks are buzzing with excitement over Gen AI, and its future in the sector looks even brighter. Banks are buzzing with excitement over Gen AI, and its future in the sector looks even brighter.

From writing assistance to automated data analysis, LLMs enable users to work more efficiently, thereby freeing up time to focus on higher-value tasks. LLMs also enable hyper-personalization, whereby recommendations, marketing messages, and user interfaces can be tailored to the preferences of each individual user.

How do banks make money? What is a bank really worth? Firstly, by outlining the major items on a bank’s income statement, and then by discussing key ratios that are commonly used to measure profitability and to estimate the market value for banks. Where does this money ultimately go?

The financial technology (fintech) phenomenon first started to evolve in the capital markets (CM) industry more than 40 years ago. This shortfall is partly due to the highly specialized and regulated nature of capital markets, which may hinder outside investors. Focus Monday, November 07, 2016.

Smart, always-connected devices and anytime/anywhere interactions are now givens, particularly among millennials, who expect such conveniences in banking and financial services. Mapping this group to its customer base, the bank can make targeted offers to customers who could be in the home or auto market in the next 30 to 90 days.

Despite many current applications being small-scale pilot projects, the promise of Gen AI to revolutionise banking operations and enhance customer experiences is becoming clear. Real-time market analysis There is a rich potential for Gen AI tools to considerably assist in strategic decision-making. Data-driven decision-making 2.1

A Simple Question about the Credit Markets. Heres my understanding of the current TARP/TARPII/PPIP/etc plans: The major "sick" banks wont lend to businesses, because their balance sheets are tied up with bad assets that they cant sell. The government will buy those assets, freeing up the major banks to loan again to businesses.

Before we dive into why AI is the solution for the banking sector, let’s first explore what big tech companies have in common, how many of them have grown successfully, and what banks can learn. Usage of AI in the Banking Sector. Table 1: AI applications across Canadian and US banks (Source: Financial Post, Techemergence).

For all the angst over the disruptive impact of financial technology providers, the smart money in corporate banking sees fintechs as strategic allies, not enemies. Over the past decade, the fintech market has become a hotbed of customer-centric banking innovation.

Blockchain has important implications for marketing and advertising. But according to The CMO Survey , only 8% of firms rate the use of blockchain in marketing as moderately or very important. This combination creates a natural barrier to entry and has likely caused marketers to take a “wait and see” approach.

Just over 10 years ago, French bank BNP Paribas froze U.S. The market panicked. There was a run on British bank Northern Rock. Over the next year, many banks fell. Investment bank Bear Stearns collapsed. We expect investment banks to embark on an even more fundamental makeover during the next decade.

This confusion originates in the fact that for older forms of money — gold or bank notes — there is no distinction between the “what” and the “how”; you simply pay by handing dollar bills or gold coins to the seller. This made traditional banks in the U.S. This made traditional banks in the U.S.

What are the Benefits of Learning & Development Programs for Organizations When you’re spending the time and money training employees, you want to ensure that you’re getting the best bank for your buck–that’s where learning and development programs come in. Why is a reduced turnover rate so important, you ask?

The Business of Banking. Banks are intermediaries for capital and hold the risk when supply and demand is not perfectly balanced. Commercial Banking. A bank, on the other hand, can diversify this credit risk and reduce the average cost of vetting each loan by lending to many borrowers. Investment Banking.

Much less emphasis has been placed on developing tools suitable for emerging markets and the businesses in these economies. Obstacles in Emerging Markets. Emerging markets face a unique challenge when it comes to deploying technology to fight COVID-19 due to the large role that informal markets play in these economies.

Two, you solve them the same way you solve a market sizing question (see below) – by breaking down the solution into component parts. . The market for lead pencils has been declining at 4%/year for the last 3 years. The original market was $24M/year. What is the market in year 3 (now)? Market Sizing.

The consumer banking industry is notoriously difficult to enter, not least because most customers rarely switch banks. In some countries, people change spouses more often than they change banks. It has now become the largest bank in the country. ShutterWorx/Getty Images. Importantly, profits kept pace.

Much has been made of the fact that a new breed of financial technology (or fintech) companies is unbundling banks in the developed world. Startups are attacking all of the components of the traditional bank value proposition (e.g., Lack of Infrastructure and Efficient Cloud Services.

One of today’s most celebrated examples of leapfrogging is the M-Pesa mobile payment system in Kenya and Tanzania, which lets people bank in their national currency using only their phones, leapfrogging traditional banking practices and creating a mobile banking revolution. The system currently serves a billion people.

My perspective and approach to misconduct risk are influenced by my work as a bank supervisor, and by my background and training as an economist. In my view, bank supervision must include attention to the culture at financial firms, not just to their financial safety and soundness. Market Failures and Misconduct Risk.

More Efficient Operations AI enables businesses to automate repetitive and time-consuming tasks, freeing up human resources to focus on more complex and strategic activities. Robotic Process Automation (RPA) is becoming widely adopted to automate manual processes, reduce errors, and increase efficiency.

FinTechs are internet companies that streamline financial systems and make funding the supply chain more efficient. They include new enterprises such as Orbian , Prime Revenue , C2FO , Taulia , and Ariba as well as new operations launched by traditional financial service firms such as Citi Group, HSBC, BNP Paribas, and Deutsche Bank.

The value of bank branches, for example, is no longer to manually process deposits, but to solve more complex customer problems like providing mortgages. market share in online sales. Once a task becomes automated, it also becomes largely commoditized. In much the same way, nobody calls a travel agency to book a simple flight anymore.

Since the advent of Bitcoin in 2008, digital currency has been a growing trend and a growing area of interest for consultants, businesses, fintech investors, central banks, and governments. Digital currency vs electronic banking. Another difference is that electronic banking involves interacting with the banking system.

A cornerstone of efficient and transparent markets is freely available information. But does the mere action of placing a piece of financial news in the public domain make it readily seen and efficiently reflected in stock prices? And reprints of old news continue to spur market reactions.

Oliver Wyman’s CEO, John Drzik, states that the long-term aspiration is to be recognized widely in the market as the gold standard in consulting. Corporate and Institutional Banking. Retail and Business Banking. They have served Global 1000 clients over the past 40 years. Surface Transportation. Public Policy.

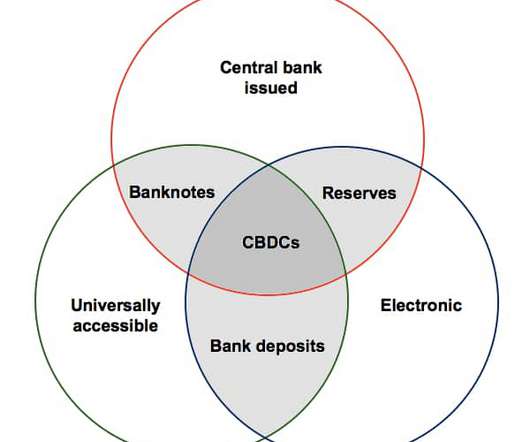

Central Bank Digital Currencies (CBDCs) are a new form of digital currency that will be issued and backed by central banks. While CBDCs and bank deposits can both be transferred digitally, there are at least five key differences between CBDCs and bank deposits that are worth being aware of.

Example: The Bank of China , " holding almost $9.7 Market Plays: In consulting and banking you find very smart, hardworking people who believe completely in capitalism, the profit motive, and proper incentives will lead to the economic dominance of whichever species best captures their motivating principles. billion (U.S.)

While the ability to authenticate identity was now digital, bank accounts and payment systems were still paper-based — requiring separate and laborious Know Your Customer validation procedures that had the result of continuing to exclude a majority of the people in India from accessing the benefits of banking.

Peer-to-peer Fundraising Email Marketing Website Management Website Design Payment Processing Sphere Know How Blog Sphere Knowledgebase Sphere Forum Case Central Sphere Connect Sphere Connect Partners Blackbaud Connect Partner Network Overview Partner Login. Non Profit Direct Marketing. Get the Flash Player to see this player. -->.

In its half-yearly global financial stability report, it said the risks to stability no longer came from the traditional banks but from the so-called shadow banking system – institutions such as hedge funds, money market funds and investment banks that do not take deposits from the public.

The market demand for these payment systems has been monumental, as the ability to pay friends and family was previously inefficient and had significant potential to be alleviated by technology. These mobile payments have completely transformed the way people manage their transactions and are increasingly becoming a standard use in America.

The partnership has been a triumph of efficiency — a win-win for the cultural climate of Judson and often-stretched student bank accounts. In a similar vein, a new group of innovators is finding efficiencies not in separating people by age but by bringing them together. But something else has happened.

And the pioneering work of social enterprises in sectors like construction , manufacturing , banking , hospitality and healthcare suggest that innovative and sustainable businesses are able to thrive without being run primarily for profit. Rise of Social Enterprise. The growing trend towards social enterprise could be a game changer.

In contrast, economies of scope is a lesser known concept particularly relevant to small and medium sized enterprises (SMEs) that may not have access to large markets or the ability to produce at scale. Economies of scope have been found to exist in a range of industries including banking, publishing, distribution, and telecommunications.

Thus a trust and efficiency engine like blockchain technology has the potential to drive radical change in the insurance industry while improving transparency and outcomes across the entire value chain. And yet trust in business institutions, and the financial services sector in particular, is at an all-time low.

International trade has tripled as a share of global GDP since 1945, and banks have done well from it. Documentary trade, traditionally facilitated by letters of credit (LCs) issued by banks, is steadily being replaced by open-account trade. Banks must be prepared to respond to rapid changes in the quantity and location of demand.

China''s Move to Market-Set Rates Let''s step back to December 8 and look at China Relaxes Grip on Interest Rates China is relaxing its grip on interest rates with the launch of a financial instrument that allows banks to trade deposits with each other at market-determined prices.

Return on assets indicates how efficient management is at using assets to generate earnings. Value is defined in the other paper according to the Tobin’s q ratio, which indicates the market value of a company’s assets. So, what’s an entrepreneur to make of these findings?

We organize all of the trending information in your field so you don't have to. Join 55,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content