This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Artificial intelligence (AI) is transforming industries across the globe, and banking is no exception. The adoption of AI is revolutionizing bankingproducts, enabling financial institutions to offer personalized service, increase efficiency, and enhance security. AI-Driven Innovations in BankingProducts 1.

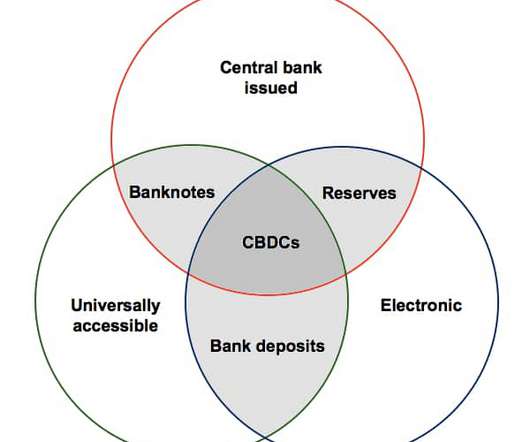

As cryptocurrency gains popularity and central bank digital currencies ( CBDCs ) are explored globally, major financial institutions are undergoing significant transformations to adapt to this new landscape. Central banks worldwide are exploring the potential of CBDCs as digital versions of their national currencies.

For product leaders , large language models (LLMs) arent just another shiny tech trend, theyre reshaping how businesses interact with customers, automate workflows, and make decisions. From writing assistance to automated data analysis, LLMs enable users to work more efficiently, thereby freeing up time to focus on higher-value tasks.

Today, I want to introduce you to (or perhaps remind you of) the concept of the minimum efficient scale. For example, Amazon is able to process and deliver its customers’ orders very efficiently because of its “scale.”. The concept of “minimum efficient scale” is less well known and is a less-used term. Minimum efficient scale.

How do banks make money? What is a bank really worth? Firstly, by outlining the major items on a bank’s income statement, and then by discussing key ratios that are commonly used to measure profitability and to estimate the market value for banks. Where does this money ultimately go?

Despite many current applications being small-scale pilot projects, the promise of Gen AI to revolutionise banking operations and enhance customer experiences is becoming clear. This helps banks to quickly identify profitable investment opportunities and risks so as to maximise investment returns and minimize losses. Risk Management 3.1

Smart, always-connected devices and anytime/anywhere interactions are now givens, particularly among millennials, who expect such conveniences in banking and financial services. Organizations have always collected data on customers, suppliers, products, and services. Digital is reconfiguring the world.

Before we dive into why AI is the solution for the banking sector, let’s first explore what big tech companies have in common, how many of them have grown successfully, and what banks can learn. Usage of AI in the Banking Sector. Table 1: AI applications across Canadian and US banks (Source: Financial Post, Techemergence).

What are the Benefits of Learning & Development Programs for Organizations When you’re spending the time and money training employees, you want to ensure that you’re getting the best bank for your buck–that’s where learning and development programs come in. Why is a reduced turnover rate so important, you ask?

Consumers are no longer swayed by just a great product, but seek more than that, craving authenticity and a genuine connection to the brand. In aB2Bcontext, your USP might focus on efficiency, cost savings, or technical performance. Indeed, the battle to build brand loyalty requires more than just great products.

Just over 10 years ago, French bank BNP Paribas froze U.S. There was a run on British bank Northern Rock. Over the next year, many banks fell. Investment bank Bear Stearns collapsed. We expect investment banks to embark on an even more fundamental makeover during the next decade. The New Face of Investment Banks.

These systems can suggest relevant products that customers are likely to enjoy. For example, businesses like Netflix, Youtube, Amazon, and Airbnb use AI-powered recommendation systems to suggest movies, videos, products, and rental properties based on a user’s browsing history, past purchases, and revealed preferences based on past behavior.

The Business of Banking. Banks are intermediaries for capital and hold the risk when supply and demand is not perfectly balanced. Commercial Banking. A bank, on the other hand, can diversify this credit risk and reduce the average cost of vetting each loan by lending to many borrowers. Investment Banking.

Much has been made of the fact that a new breed of financial technology (or fintech) companies is unbundling banks in the developed world. Startups are attacking all of the components of the traditional bank value proposition (e.g., Lack of Infrastructure and Efficient Cloud Services. Sidian Bank in Kenya has a similar program.

The consumer banking industry is notoriously difficult to enter, not least because most customers rarely switch banks. In some countries, people change spouses more often than they change banks. It has now become the largest bank in the country. These areas were underserved by the traditional banks.

But this is the story of how a group of bank examiners at the Federal Reserve Bank of Philadelphia, one of 12 banks in the U.S.’s The 250 people in the supervision, regulation, and credit group at the Philadelphia bank supervise the commercial and retail banks based in their district.

” “ He owns a big share of the company, and of course he wants to increase the production volume to raise the profitability and expand.” Approved checking account/bank overdraft facilities: the approved overdraft credit. ” “ He is looking for a company to buy. That shows some guts to grow.”

Economies of scope exist where a firm can produce two products at a lower per unit cost than would be possible if it produced only the one. If properly understood, economies of scope could be used by SMEs to drive profit growth and reduce the risk associated with product failure. Importance. burgers, fries, sundaes and salads).

Let’s start by examining the potential effects of this on an industry that touches all of our lives – banking. The banking industry is filled with shared resources. Instead, the technology itself would do the heavy lifting of uniting the interests and business processes of the member banks.

The war certainly has prevented an efficient economic structure, forcing many Colombians to be inward-looking. Banks often are unwilling to take the risk of financing small and midsize companies. TFP, a measure of efficiency of labor and capital inputs, has actually declined for the past seven years.

The value of bank branches, for example, is no longer to manually process deposits, but to solve more complex customer problems like providing mortgages. Once a task becomes automated, it also becomes largely commoditized. Value is then created on a higher level than when people were busy doing more basic things.

Give me an example of a good product and not so good product. This product management (PM) interview question tests whether you understand product design principles. Is your evaluation of products guided by principles of good design? Define the design principles behind the success of this product.

My perspective and approach to misconduct risk are influenced by my work as a bank supervisor, and by my background and training as an economist. In my view, bank supervision must include attention to the culture at financial firms, not just to their financial safety and soundness. The economics of corporate culture. Externalities.

Heres my understanding of the current TARP/TARPII/PPIP/etc plans: The major "sick" banks wont lend to businesses, because their balance sheets are tied up with bad assets that they cant sell. The government will buy those assets, freeing up the major banks to loan again to businesses. The question would be: which bank is not sick?

“Productivity isn’t everything, but in the long run it is almost everything,” wrote Paul Krugman more than 20 years ago. Productivity in most developed economies has been anemic. During much of this time, it has been shareholders, not workers, who have reaped the benefits of higher productivity.

They seized this opportunity to establish a firm that would help firms gain clarity about their business models, products, and clients and then advise them by creating long term strategies. Industrial Products. Retail and Consumer Products. Corporate and Institutional Banking. Retail and Business Banking.

FinTechs are internet companies that streamline financial systems and make funding the supply chain more efficient. They include new enterprises such as Orbian , Prime Revenue , C2FO , Taulia , and Ariba as well as new operations launched by traditional financial service firms such as Citi Group, HSBC, BNP Paribas, and Deutsche Bank.

Since the advent of Bitcoin in 2008, digital currency has been a growing trend and a growing area of interest for consultants, businesses, fintech investors, central banks, and governments. Digital currency vs electronic banking. Another difference is that electronic banking involves interacting with the banking system.

Recently, the CEO of Deutsche Bank predicted that half of its 97,000 employees could be replaced by robots. ” And for those in manufacturing or production companies, the future may arrive even sooner. ” The point of technology, she argues, is to boost productivity, not cut the workforce. Insight Center.

However, in business, decisions can be effectively and efficiently made based on near-perfect data/calculations. The framework should be in 2 levels , and beyond revenues and costs it could highlight a potential internal company or product problem, competition or a global market issue, etc. Post Office for mailing needs versus UPS.

For example, online retailers can adjust product prices daily because they have automated the collection of competitors’ prices. With automated pricing engines, insurers and banks can roll out new offers as fast as online competitors. Meanwhile, companies that automate basic data manipulation processes can be proactive.

The partnership has been a triumph of efficiency — a win-win for the cultural climate of Judson and often-stretched student bank accounts. In an HBR article , two management school professors found that an age-integrated assembly line resulted in improved productivity, reduced absenteeism, and fewer defects.

You’re probably familiar with the “minimum viable product” of Eric Ries’ Lean Start-Up fame; but here I’m talking about the acronymically identical “minimum viable pilot.” ” A fintech start-up enjoyed greater success piloting a security offering with a global bank. ” Insight Center.

Digital technologies are reshaping the banking industry at an unprecedented rate, generating waves of fresh opportunity and potential peril for traditional banks. Digital has increased customers’ expectations for greater efficiency, quality, and speed, and it has opened the door to new competitors and disruption.

BCG’s Retail-Banking Excellence benchmarking study (REBEX) profiles the operational and digital practices and performance of 20 of the world’s leading retail banks, a group of 40 institutions chosen for their size and the strength of their capabilities. We refer to these banks as the “premier league.”

And the pioneering work of social enterprises in sectors like construction , manufacturing , banking , hospitality and healthcare suggest that innovative and sustainable businesses are able to thrive without being run primarily for profit. Rise of Social Enterprise. The growing trend towards social enterprise could be a game changer.

As a startup founder, I’m constantly struggling to recruit top talent without breaking the bank. And it shrinks the gap between cash going out and coming in for the company since you’re often not paying out the money until the additional revenue is banked. HBR Staff/Phatharapol Nopharat/EyeEm/Getty Images.

Low transaction costs will also be necessary to ensure efficient operations and to ensure that blockchain systems offer a cost advantage over the status quo. Supply chain tracking also makes it possible to pinpoint the origins of products, and so ensure that goods are sourced from safe and sustainable suppliers.

Example: The Bank of China , " holding almost $9.7 Market Plays: In consulting and banking you find very smart, hardworking people who believe completely in capitalism, the profit motive, and proper incentives will lead to the economic dominance of whichever species best captures their motivating principles. Productivity. (6).

When Bernstein hid a set of production lines from managers’ view, the performance of employees on those lines increased by 10% to 15%. A great salesperson will operate much more efficiently with a defined process for reaching out to prospects. They will represent the products more consistently. Building Balanced Cultures.

And that’s not just social media accounts; it’s bank accounts, retailer gift card accounts with cash and credit cards attached, airline loyalty accounts with years of accumulated frequent flyer points, and other accounts with real value. Over three billion credentials were reported stolen last year.

.” Plus, parenting has almost certainly taught you important lessons about multitasking, negotiation, persuasion, and stress management — and that may, in fact, make you a more productive and well-rounded employee. Research by the Federal Reserve Bank of St. Fifth and finally, don’t get discouraged.

The landscape of retail banking is rapidly changing. Physical banks are closing and the age of virtual banking is here. It is causing banks and financial services firms to adapt to a whole new way to provide personalized services. The shift to virtual banking.

We organize all of the trending information in your field so you don't have to. Join 55,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content